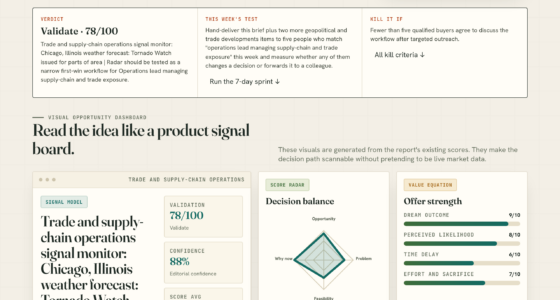

📊 Full opportunity report: The labor share. Is value really moving from labor to capital? The data isn’t on anyone’s side yet. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

The debate over whether AI is moving value from labor to capital remains unresolved. While the overall labor share has been stable for decades, early signals suggest shifts at the margins, making the issue complex and uncertain.

Recent data confirms that the US labor share of income has remained within a narrow range of 57 to 64 percent over the past 70 years, despite technological changes including AI. However, early signals suggest that at the margins, particularly among entry-level workers, AI may be beginning to shift value from labor to capital, creating a complex and unresolved picture.

The long-term data indicates that the aggregate labor share has been remarkably stable since the 1950s, despite waves of automation, digitalization, and technological innovation. This stability challenges claims that AI is currently redistributing income from labor to capital on a broad scale. However, recent studies, including a Stanford analysis of millions of payroll records, show a roughly 13 percent decline in employment for 22-to-25-year-olds in AI-exposed occupations since late 2022, even after controlling for firm shocks. This suggests a displacement at the entry-level or routine cognitive work that AI automates first, aligning with theoretical predictions. The core debate centers on whether these marginal signals will eventually translate into a sustained, economy-wide shift in the labor share. Proponents argue that the early signs of displacement and regional declines in Europe indicate a process that could lead to a broader redistribution of income, while skeptics note that the stable aggregate data over decades suggests resilience and reallocation within the labor force rather than a fundamental shift in value distribution.The labor share.

Is value really moving

from labor to capital?

The data isn’t on

anyone’s side yet.

the skeptic’s strongest chart

in AI-exposed jobs since 2022 (Stanford)

declining labor share (Minniti et al.)

confirmable only in retrospect

The empirical ambiguity that weakens a confident displacement narrative is precisely what strengthens the case for a response that doesn’t require the narrative to be confident. You don’t need the premise proven to justify a no-regrets response. You only need it plausible — and the marginal evidence makes it more than plausible.Thorsten Meyer · The Labor Share · Post-Labor 02

This debate matters because it influences policy decisions on ownership, redistribution, and economic resilience. If AI is beginning to shift value from labor to capital at the margins, it could justify policies promoting broad ownership of productive assets to protect workers. Conversely, if the overall labor share remains stable, immediate policy changes may be less urgent. The core issue is understanding whether the signals at the edges reflect a temporary phase or a long-term trend, which remains uncertain at this point.

AI automation workforce training courses

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Since the 1950s, the US labor share of income has fluctuated within a narrow band, despite technological revolutions like automation, the internet, and digitalization. Historically, the labor share has shown resilience, with workers reabsorbing displaced jobs and adjusting wages. Recent studies, including a Stanford report, highlight early signs of displacement among young workers in AI-exposed fields, raising questions about whether this pattern signals a future shift or is part of normal labor market dynamics. The debate hinges on whether these marginal signals will accumulate into a significant, long-term redistribution of income.

“The stable aggregate labor share over 70 years suggests resilience, but early signals at the margins indicate a potential shift that is not yet reflected in the overall data.”

— Thorsten Meyer

Elgato Stream Deck Mini – Control Zoom, Teams, PowerPoint, MS Office and More, Boost Productivity with Seamless Integration for Daily Apps, Set Up Shortcuts Easily, Compatible with Mac and PC

Work smarter not harder: forget keyboard shortcuts. Stream Deck Mini lets you assign tedious, hard to memorise shortcuts…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unresolved Questions About Long-Term Impact

It remains unclear whether the early marginal signals will develop into a sustained, economy-wide shift in the labor share. The aggregate data has not yet shown a significant decline, and the timing of any potential shift is uncertain. The relationship between current displacement and long-term value redistribution is still being studied, and more data over time is needed to clarify this trend.

Key Labor Market Indicators: Analysis with Household Survey Data (Streamlined Analysis with ADePT Software)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Monitoring Data and Policy Responses in the Coming Years

Researchers will continue analyzing labor market data, especially at the margins, to determine if the early signals persist or intensify. Policymakers are advised to consider responses that are robust to uncertainty, such as promoting broad-based ownership of productive assets, which could mitigate potential future shifts regardless of whether the aggregate labor share begins to decline. The passage of time and accumulating evidence will be critical in clarifying the long-term trend.

Income and Expense Log Book – Bookkeeping Record Book/Tracker/Small Business Ledger Book & Accounting, 8.5" x 10.5", Undated Record Book& Business Ledger, Durable Polypropylene Cover(Red)

Income And Expense Log Book: This Income and Expense Record Book(8.5" x 10.5") is a necessary item for…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Is the labor share currently decreasing overall?

No, the data shows that the US labor share has remained within a narrow range of 57 to 64 percent over the past 70 years, despite technological changes.

What are the early signs that AI might be shifting value?

Recent studies, including a Stanford analysis, point to a decline in employment among young workers in AI-exposed roles and regional labor-share declines, suggesting displacement at the margins.

Not necessarily. Stability at the aggregate level can mask displacement at the margins or within specific sectors. Early signals suggest some groups and roles are experiencing shifts.

Why is it difficult to determine if a long-term shift is happening?

Because the labor share is only definitively measurable after the fact, and current data captures early signals that may or may not develop into a lasting trend.

What policy options are suggested given this uncertainty?

Policies promoting broad ownership of productive assets and protecting workers at the margins are recommended, as they are robust responses to uncertain long-term shifts.

Source: ThorstenMeyerAI.com